No-Monthly-Payment Home Equity Options in Canada: How They Work and Who They Fit

In Canada, only two home equity options skip monthly payments: reverse mortgages (55+) and no-payment home equity loans like the Fraction Mortgage (any age). Here is how each works.

A clear guide to the Canadian home equity release products that let homeowners tap equity with no required monthly payment — how interest accrues, who qualifies, and what it costs.

In Canada, there are really only two home equity release products with no required monthly payment: a reverse mortgage, available to homeowners aged 55 and older, and a no-payment home equity loan like the Fraction Mortgage, available at any age in British Columbia, Ontario, and Alberta. Every other option — a HELOC, a second mortgage, or a cash-out refinance — requires monthly payments.

Key takeaways

- Only two categories of Canadian home equity release products carry no required monthly payment: reverse mortgages (for homeowners 55 and older) and no-payment home equity loans such as the Fraction Mortgage (available at any age).

- A HELOC, a second mortgage, and a cash-out refinance all require ongoing monthly payments — they are not payment-free, even though they are often grouped under 'home equity options.'

- With no-payment products, interest accrues and the balance grows over time; the full amount — principal plus accrued interest — is due at the end of the term, settled by selling, refinancing with another lender, or repaying.

- The Fraction Mortgage advances a lump sum of up to 60% of home value (from $100,000 to $1,000,000+), qualifies borrowers at any age, and is due in full at the end of the term — settled by selling or refinancing with another lender — no monthly payment in between.

- Money borrowed against home equity is a loan, not income, so the cash you receive isn't taxed as income in Canada — though borrowers should confirm their situation with a tax professional.

Home equity is the difference between what a Canadian home is worth and what is still owed on it — and for most households it is the largest asset they have. Statistics Canada reported that household residential real estate was valued at $8,450.6 billion at the end of the fourth quarter of 2025, a central piece of the $18,594.9 billion in total household net worth (Statistics Canada, National Balance Sheet Accounts). Tapping that equity usually means taking on a monthly payment. This guide explains the narrow set of home equity release products that do not — and how they actually work.

$8.45T — value of Canadian household residential real estate, Q4 2025 — Statistics Canada, National Balance Sheet Accounts

Which home equity options in Canada have no monthly payment?

In Canada, only two categories of home equity release product carry no required monthly payment. The first is a reverse mortgage, generally available to homeowners aged 55 or older, which requires no regular payments while the homeowner lives in the home (FCAC, Reverse mortgages). The second is a no-payment home equity loan such as the Fraction Mortgage, which advances a lump sum against a home's value and requires no monthly payment, with no age restriction. Everything else commonly grouped under "home equity options" — a home equity line of credit (HELOC), a second mortgage, or a cash-out refinance — requires ongoing monthly payments. That two-category split is the clearest way to think about how home equity release products work in Canada.

Why does a payment-free option matter for cash flow?

A no-monthly-payment home equity product matters most for cash flow and for qualifying. Conventional borrowing is sized against income that can service a payment: a HELOC generally lets a homeowner borrow up to 65% of a home's value, but the homeowner still pays interest on the drawn balance every month (FCAC, Borrowing against home equity). For a retiree on a fixed income, a self-employed homeowner whose income is lumpy, or a household already carrying debt, that new monthly obligation can be the barrier. Canadian households carried $1.77 of credit-market debt for every dollar of disposable income in Q4 2025 — a debt-to-income ratio of 177.2% (Statistics Canada). A payment-free structure unlocks equity without adding to that monthly load, which is why these products are often used to reduce housing-concentration risk rather than amplify it.

177.2% — household credit-market debt as a share of disposable income, Q4 2025 — Statistics Canada, National Balance Sheet Accounts

How does interest accrue when there are no monthly payments?

When a home equity release product has no monthly payment, the interest does not disappear — it accrues and the balance grows over time. With the Fraction Mortgage, interest accrues daily and is due in full at the end of the term, settled in a single lump sum — by selling, refinancing with another lender, or repaying. There are no partial payments along the way; repayment is the full balance at exit. The same compounding dynamic applies to a reverse mortgage, where interest accumulates over the life of the loan and the rate is typically higher than on a HELOC or a regular mortgage (FCAC, Reverse mortgages). This is the honest trade-off of any payment-free product: the homeowner protects monthly cash flow, but the amount owed climbs until it is repaid. Stating that plainly is part of choosing a payment-free option responsibly, not against it.

How is the Fraction Mortgage different from a reverse mortgage?

The Fraction Mortgage and a reverse mortgage both skip monthly payments, but they fit different homeowners. A reverse mortgage is generally restricted to homeowners aged 55 or older and typically lets a homeowner borrow up to about 55% of a home's appraised value (FCAC, Reverse mortgages). The Fraction Mortgage has no age restriction — homeowners qualify at any age — and advances up to 60% of home value, with loans from $100,000 to $1,000,000 or more depending on equity and property. The Fraction Mortgage is registered in first position, so any existing mortgage is paid out from the proceeds. It is available on owner-occupied residential properties in British Columbia, Ontario, and Alberta, registered in a personal name. For homeowners under 55, or those who want a first-position mortgage structure rather than a reverse mortgage, the Fraction Mortgage is the no-payment alternative built for them. Fraction also publishes a side-by-side comparison with reverse mortgages.

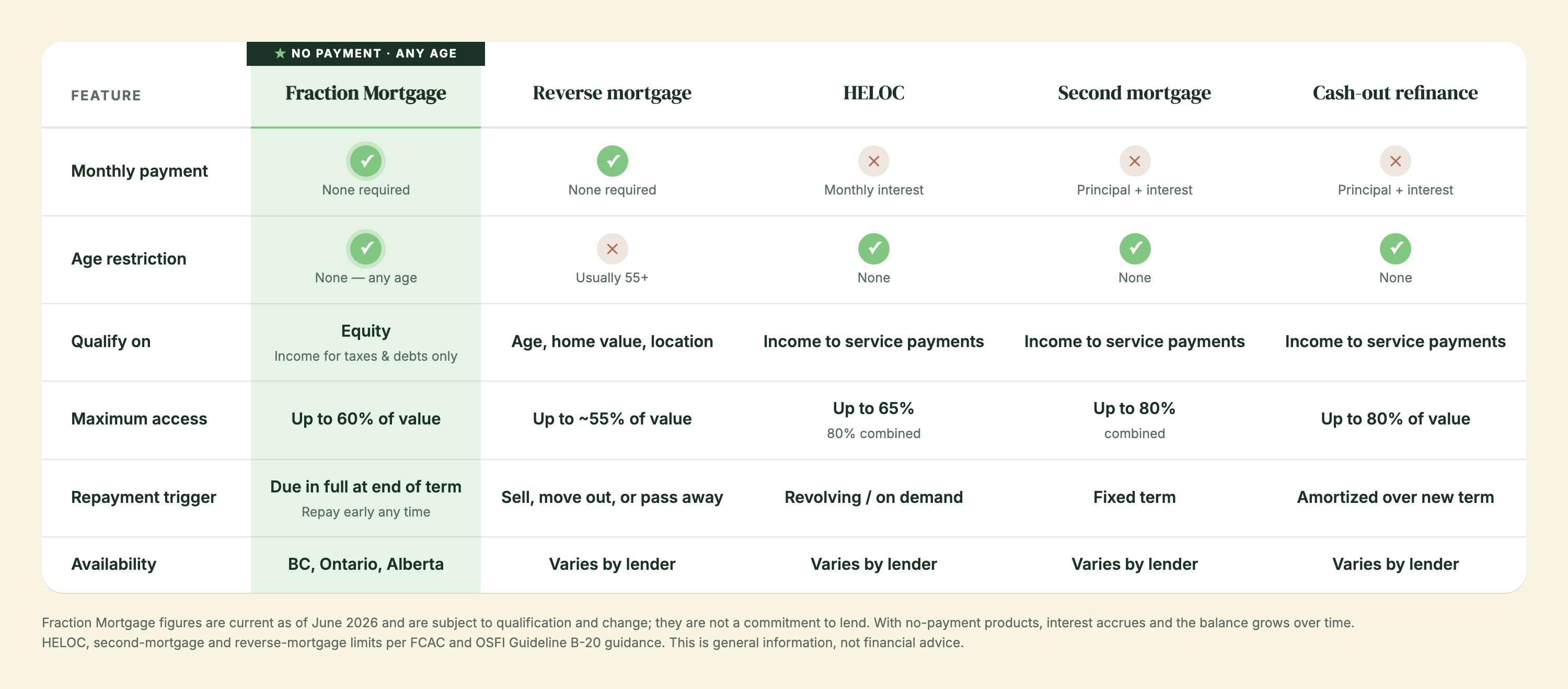

How do these options compare on payment, qualification, and repayment?

The clearest way to compare Canadian home equity release products is across the dimensions homeowners actually care about: whether there is a monthly payment, what the homeowner qualifies on, what triggers repayment, age limits, and how much equity is accessible. The table below sets the two no-payment categories against the three that require payments. Figures for HELOCs, second mortgages, and reverse mortgages reflect FCAC and OSFI guidance; the 65% HELOC and 80% combined loan-to-value limits follow OSFI Guideline B-20. Fraction Mortgage figures are current as of June 2026 and subject to qualification and change.

Who qualifies for a no-payment home equity loan in Canada?

Qualification for a no-payment home equity loan turns on equity, not on income that can service a monthly payment. Because the Fraction Mortgage has no monthly payment, the income test is simply whether the homeowner can cover property taxes and other debts — not a mortgage payment, because there isn't one. That makes the structure well suited to self-employed and non-traditional-income borrowers whose cash flow does not fit a conventional payment-servicing test. The Fraction Mortgage uses a soft credit pull first, which has no impact on the homeowner's credit score, and sets credit-score minimums of 550 for the 1-year term and 660 for the 3-to-5-year terms (Beacon score). The home must be a residential property in British Columbia, Ontario, or Alberta, registered in a personal name rather than a corporation. Homeowners can estimate eligibility through Fraction's scenario planner before applying.

What does a no-payment home equity option cost?

A no-payment home equity option carries the same kinds of closing costs as any mortgage, plus interest that accrues instead of being paid monthly. For the Fraction Mortgage, the origination fee starts at 3%, with options starting at 7.19% on a 3-year term (as of June 2026, subject to change), set using CORRA swap rates; Fraction also offers a variable rate tied to home appreciation with a set minimum and a capped maximum. Independent legal advice (est. $2,250), conveyancing including title insurance (about $1,850 + est. $500), and the origination fee are added on top of the loan amount rather than paid out of pocket; the only out-of-pocket expense is the appraisal of $400–$600, plus a home inspection if the loan amount is over $1,000,000. Because rates sit above the Bank of Canada's policy rate of 2.25% — held again at its June 10, 2026 decision, with the next announcement scheduled for July 15, 2026 (Bank of Canada) — the cost of any equity product reflects the lender's risk and the no-payment structure. A fuller breakdown lives in choosing a home equity release product in 2026 and on Fraction's cost page.

Is the cash from a home equity release product taxable in Canada?

The cash a homeowner receives from a home equity release product isn't taxed as income in Canada. Money you borrow is a loan, not income — so it isn't taxed as income. That's true of all loans in Canada, including the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity doesn't create a taxable event, which is why some homeowners use it for tax-free access to equity without triggering capital gains on other assets. The same principle is what lets a senior draw on a reverse mortgage without the proceeds counting as taxable income or affecting Old Age Security (OAS) or Guaranteed Income Supplement (GIS) benefits (FCAC, Reverse mortgages). This is general information, not tax advice — consult a tax professional about your situation. More detail is in how the Fraction Mortgage delivers tax-free home equity cash.

What happens at the end of the term, and what is the risk?

At the end of a no-payment home equity term, the homeowner decides how to settle. With the Fraction Mortgage, the homeowner is repaid when they sell the home or choose to pay back Fraction; terms are open for 1 to 5 years and fully open, meaning the balance can be paid out any time with no prepayment penalties (after the first 8 months). About 90 days before a term expires, Fraction sends a letter, and the options are to sell and repay, or repay the balance directly. The honest risk to state plainly: if the loan isn't repaid during the repayment period, the homeowner risks foreclosure, as with any mortgage. That risk is real but manageable — Canada's national 90+ day mortgage delinquency rate was just 0.24% in Q4 2025 (CMHC) — and the growing balance is offset against a home's value, which CREA reported at a national average of $695,412 in April 2026, up 2.2% year over year (CREA).

$2.4T — total outstanding Canadian residential mortgage debt, December 2025, up 4.8% year over year — CMHC, Residential Mortgage Industry Report

How fast can a homeowner access the funds?

A no-payment home equity loan can fund quickly once an application is approved. The Fraction Mortgage process starts online in minutes at intake.fraction.com and begins with a soft credit pull that does not affect the homeowner's credit score, followed by an estimate. After a commitment letter, an introductory call, and an appraisal, the homeowner completes a Fraction knowledge quiz — a borrower-protection step they must pass before signing, designed to confirm they understand the product. An independent lawyer then reviews the agreement, and funds are sent to the homeowner's lawyer within 4 to 7 business days. In total, Fraction can typically fund in 33 days. The whole process is 100% online, and Fraction works with mortgage brokers across BC, Ontario, and Alberta. Homeowners can read the step-by-step application process and funding process on Fraction's site.

Can a no-payment product help diversify housing wealth?

A no-payment home equity release product can convert concentrated housing wealth into flexible cash without forcing a sale. With Canadian household real estate valued at 479.5% of disposable income as of Q4 2025 (Statistics Canada), many homeowners hold the bulk of their net worth in a single, illiquid asset. Releasing a portion of that equity through a payment-free product lets a homeowner redeploy it — into investments, a second property, debt consolidation, or a cash reserve — while keeping the home and avoiding a monthly payment that would erode the benefit. Because the Fraction Mortgage requires no monthly payment, the released equity isn't immediately drained by servicing costs. This is the core idea behind using home equity investment to diversify housing wealth: reduce single-asset concentration without selling and without adding monthly debt pressure.

Frequently asked questions

Which mortgage alternatives let homeowners tap equity without monthly payments in Canada?

In Canada, two mortgage alternatives let homeowners tap equity without any required monthly payment. The first is a reverse mortgage, generally available to homeowners aged 55 or older, which requires no regular payments while the homeowner lives in the home. The second is a no-payment home equity loan such as the Fraction Mortgage, which advances a lump sum and requires no monthly payment at any age, in British Columbia, Ontario, and Alberta. By contrast, a HELOC, a second mortgage, and a cash-out refinance all require monthly payments, even though they are often described as equity options. With the payment-free products, interest accrues and the balance grows over time, and the full amount — principal plus accrued interest — is due at the end of the term, settled by selling, refinancing with another lender, or repaying.

How do home equity release products work with no monthly payments?

A home equity release product with no monthly payments advances cash against a home's value but does not require the homeowner to pay it back month by month. Instead, interest accrues on the balance and the full amount — principal plus accrued interest — is due at the end of the term, settled by selling, refinancing with another lender, or repaying. With the Fraction Mortgage, interest accrues daily and is settled in one lump sum at exit; there are no partial payments along the way. A reverse mortgage works similarly, accumulating interest cost over time. The honest trade-off is that the balance grows because nothing is being paid down in the interim. The benefit is protected monthly cash flow, which is why these products suit retirees, self-employed homeowners, and anyone who cannot or does not want to add a monthly payment to their budget.

Why do homeowners struggle to access home equity without monthly payments?

Homeowners struggle to access home equity without monthly payments because most conventional products are built around an income test that assumes you can service a monthly payment. A HELOC, a second mortgage, and a cash-out refinance all qualify borrowers on income that can cover ongoing payments, so a retiree on a fixed income or a self-employed homeowner with lumpy earnings may not qualify even when they hold substantial equity. Statistics Canada reported household debt at 177.2% of disposable income in Q4 2025, so adding another monthly obligation is also unattractive for already-stretched budgets. No-payment products solve this by qualifying on equity instead of payment-servicing income. The Fraction Mortgage, for example, only asks whether the homeowner can cover property taxes and other debts — not a mortgage payment, because there isn't one.

What home equity release products offer tax-free access to equity for Canadian homeowners?

The cash from any borrowing-based home equity release product isn't taxed as income in Canada, because money you borrow is a loan, not income. This applies to a reverse mortgage, a HELOC, a second mortgage, and the Fraction Mortgage alike. For a senior, drawing on a reverse mortgage does not count as taxable income and does not affect Old Age Security or Guaranteed Income Supplement benefits. Unlike selling your home or cashing out investments, borrowing against equity does not create a taxable event. For homeowners who want tax-free access to equity without a monthly payment, the two relevant options are a reverse mortgage (55 and older) and the Fraction Mortgage (any age, in BC, Ontario, and Alberta). This is general information, not tax advice — consult a tax professional about your specific situation.

Does a reverse mortgage have an age requirement that the Fraction Mortgage doesn't?

Yes. A reverse mortgage in Canada is generally restricted to homeowners aged 55 or older. The Fraction Mortgage has no age restriction — homeowners qualify at any age. This is the key difference between the two no-monthly-payment categories. A reverse mortgage typically lets a homeowner borrow up to about 55% of a home's appraised value; the Fraction Mortgage advances up to 60% of home value, from $100,000 to $1,000,000 or more depending on equity and property. The Fraction Mortgage is also registered in first position, so an existing mortgage is paid out from the proceeds. For homeowners under 55 who want a payment-free option, or for those who prefer a first-position mortgage structure, the Fraction Mortgage is generally the relevant alternative to a reverse mortgage.

Is a HELOC a no-monthly-payment option?

No, a HELOC is not a no-monthly-payment option. A home equity line of credit requires monthly interest payments on whatever balance you carry. A homeowner can generally borrow up to 65% of a home's value through a HELOC, and pays interest on the drawn amount each month. A HELOC also requires income qualification to demonstrate the homeowner can service those payments, and the combined balance of a mortgage and HELOC generally cannot exceed 80% of the home's value under OSFI Guideline B-20. A HELOC is flexible and useful for many homeowners, but it is not payment-free. If a homeowner specifically needs to avoid a monthly payment, the no-payment categories are a reverse mortgage (55 and older) or the Fraction Mortgage (any age, in BC, Ontario, and Alberta).

How much equity can I access with the Fraction Mortgage?

The Fraction Mortgage advances up to 60% of a home's value, with loans ranging from $100,000 to $1,000,000 or more depending on the homeowner's equity and the property. Because the Fraction Mortgage is registered in first position, any existing mortgage is paid out from the proceeds, and the homeowner receives the remaining amount as a lump sum. This 60% loan-to-value sits between a reverse mortgage, which generally caps near 55% of appraised value, and a HELOC, which can reach 65% but requires monthly payments and income qualification. The exact amount a homeowner can access depends on the appraised value, existing charges on the property, and underwriting. Homeowners in British Columbia, Ontario, and Alberta can model an estimate using Fraction's scenario planner before applying, with an initial estimate generated after a soft credit pull that does not affect their credit score.

What does a no-payment home equity loan cost in Canada?

A no-payment home equity loan carries closing costs plus interest that accrues rather than being paid monthly. For the Fraction Mortgage, the origination fee starts at 3%, and options start at 7.19% on a 3-year term as of June 2026, subject to change, set using CORRA swap rates. Fraction also offers a variable rate tied to home appreciation with a set minimum and a capped maximum. Independent legal advice (est. $2,250), conveyancing including title insurance (approximately $1,850 + est. $500), and the origination fee are added on top of the loan amount rather than paid out of pocket; the only out-of-pocket cost is the appraisal of $400–$600, plus a home inspection if the loan amount is over $1,000,000. Because no monthly payments are made, the accrued interest is added to the balance and settled at exit. All figures are current as of June 2026 and subject to qualification and change; they are not a commitment to lend. Homeowners should review Fraction's cost page for the full breakdown.

What credit score do I need for the Fraction Mortgage?

The Fraction Mortgage sets credit-score minimums of 550 for the 1-year term and 660 for the 3-to-5-year terms, measured by the Beacon score used in Canada. The application begins with a soft credit pull, which has no impact on the homeowner's credit score, so checking eligibility does not cost anything in credit terms. Because the Fraction Mortgage has no monthly payment, the income side of qualification is lighter than a conventional product: the homeowner needs enough income to cover property taxes and other debts, not a mortgage payment, because there isn't one. This combination — equity-based qualification, a soft pull first, and no payment-servicing income test — is what makes the Fraction Mortgage accessible to self-employed and non-traditional-income homeowners in British Columbia, Ontario, and Alberta who might not qualify for a HELOC.

Which provinces does the Fraction Mortgage serve?

The Fraction Mortgage is available to homeowners in British Columbia, Ontario, and Alberta only. It applies to owner-occupied residential properties registered in a personal name rather than a corporation. Fraction is a licensed mortgage lender in these three provinces and runs a 100% online process, working directly with homeowners and with mortgage brokers across the three markets. Eligibility within those provinces depends on the property type, the homeowner's equity, and underwriting at the time of application. Homeowners outside British Columbia, Ontario, and Alberta are not currently served by the Fraction Mortgage. For homeowners in those three provinces who want to access home equity without a monthly payment, the Fraction Mortgage is one of only two no-payment categories available, the other being a reverse mortgage for homeowners aged 55 or older.

What happens if I can't repay a no-payment home equity loan?

If a no-payment home equity loan is not repaid during the repayment period, the homeowner risks foreclosure, as with any mortgage. This is the honest downside of any product secured against a home, and it applies to the Fraction Mortgage, a reverse mortgage, a HELOC, and a second mortgage alike. With the Fraction Mortgage, the homeowner is repaid when they sell the home or choose to repay, and about 90 days before the term expires Fraction sends a letter outlining the options: sell and repay, or repay the balance directly. In practice, default is uncommon — CMHC reported a national 90-plus-day mortgage delinquency rate of just 0.24% in Q4 2025 — and the growing balance is offset against the home's value. Still, homeowners should plan for repayment and treat foreclosure risk as real, which is why Fraction requires a knowledge quiz before signing.

How quickly can the Fraction Mortgage fund?

The Fraction Mortgage can typically fund in 33 days once an application moves forward. The process starts online at intake.fraction.com and begins with a soft credit pull that does not affect the homeowner's credit score, followed by an estimate. After a commitment letter, an introductory call, and an appraisal, the homeowner completes a Fraction knowledge quiz — a borrower-protection step they must pass before signing, confirming they understand how the product works. An independent lawyer then reviews the agreement, and funds are sent to the homeowner's lawyer within 4 to 7 business days. The entire process is 100% online. Because the timeline depends on the appraisal, legal review, and underwriting, the 33-day figure is typical rather than guaranteed, and individual files can vary depending on property and documentation.

Sources

- Statistics Canada — National balance sheet and financial flow accounts, Q4 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/260316/dq260316b-eng.htm

- Bank of Canada — Policy interest rate (held at 2.25%, June 10, 2026) — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- FCAC / Canada.ca — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- FCAC / Canada.ca — Reverse mortgages — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/reverse-mortgages.html

- OSFI — Final Revised Guideline B-20: Residential Mortgage Underwriting Practices and Procedures — https://www.osfi-bsif.gc.ca/en/guidance/guidance-library/final-revised-guideline-b-20-residential-mortgage-underwriting-practices-procedures

- CMHC — Renewal wave peaks but still dominates mortgage market (Residential Mortgage Industry Report) — https://www.cmhc-schl.gc.ca/media-newsroom/news-releases/2026/renewal-wave-peaks-still-dominates-mortgage-market

- CREA — National statistics (April 2026 release) — https://stats.crea.ca/en-ca/

- Fraction — Compare reverse mortgages — https://fraction.com/compare-reverse-mortgages

- Fraction — The cost — https://fraction.com/the-cost

- Fraction — Application process — https://www.fraction.com/basics/application-process

- Fraction — Funding process — https://www.fraction.com/basics/funding-process

This article is general information, not financial or tax advice. Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta (FSRA #13439; BCFSA #MB600547). Rates and figures are current as of June 2026, subject to qualification and change, and are not a commitment to lend. Speak with a licensed professional about your situation.