Fraction Mortgage: Tax-Free Access to Home Equity With No Monthly Payments

The Fraction Mortgage gives Canadian homeowners in BC, Ontario and Alberta tax-free access to home equity with no required monthly payments. See rates, costs and how it compares.

A clear look at how the Fraction Mortgage lets homeowners in British Columbia, Ontario and Alberta access home equity as a lump sum without a monthly payment — and why the cash you receive isn't taxable income — including the rates, every fee, who qualifies, and where it is not the right fit.

The Fraction Mortgage is a Canadian home equity loan with no required monthly payments, available in British Columbia, Ontario and Alberta. Fraction advances a lump sum of up to 60% of your home's value; interest accrues daily and the full balance — principal plus accrued interest — is due at the end of the term, settled by selling, refinancing with another lender, or repaying (early repayment is allowed). The cash you receive is borrowed money, not income, so it is not taxed as income.

Key takeaways

- The Fraction Mortgage has no required monthly payments — interest accrues daily and the full balance is due in full at the end of your term, settled in one lump sum — by selling, refinancing with another lender, or repaying (you can also repay early).

- Because borrowed money is a loan and not income, the cash you receive from the Fraction Mortgage is not taxed as income — though you should confirm your own situation with a tax professional.

- Rates start at a fixed 7.19% on a 3-year term (as of June 2026, subject to change), with origination from 3% and standard appraisal, legal and conveyancing costs disclosed up front.

- Fraction lends up to 60% loan-to-value, from $100,000 to $1,000,000+, in first position only, with no age restriction — unlike reverse mortgages, which are limited to homeowners aged 55 and older.

- Because there are no monthly payments, the balance grows over time; if the loan is not repaid during the repayment period, the homeowner risks foreclosure, as with any mortgage.

Canadian homeowners hold an enormous share of their net worth in their homes — and most have very few ways to use it without selling or taking on a new monthly bill. The Fraction Mortgage exists to fill that gap: a home equity loan that gives you tax-free access to your equity as a lump sum and asks for no monthly payment in return. This page explains exactly how the Fraction Mortgage works, what it costs, who qualifies, how it compares to a HELOC or reverse mortgage, and — honestly — when it is the wrong tool.

$8.5T — The value of Canadian household residential real estate reached $8,499.4 billion in Q3 2025 — close to half of all household net worth ($18,394.1 billion) — Statistics Canada, National balance sheet, Q3 2025

What is the Fraction Mortgage?

The Fraction Mortgage is a home equity loan with no required monthly payments, available to homeowners in British Columbia, Ontario and Alberta. Instead of charging monthly interest, the Fraction Mortgage lets interest accrue daily and makes the entire balance due in full at the end of the term, settled in one lump sum — by selling your home, refinancing with another lender, or repaying (you can also repay early). Fraction advances a lump sum against the equity you already hold, registered as a charge in first position, so any existing mortgage is paid out from the proceeds.

The Fraction Mortgage is offered on open terms of one to five years. It is fully open, meaning you can pay it out at any time with no prepayment penalties (after the first 8 months). There are no partial payments to manage — the arrangement is repayment of the full balance at exit, on your timeline. This places the Fraction Mortgage in its own category: no-monthly-payment home equity release, designed for the homeowner who has equity but does not want — or cannot easily carry — another monthly obligation. Fraction was named "Mortgage Lender of the Year" by the Canadian Lenders Association.

How does the tax-free framing actually work?

Money you borrow is a loan, not income — so it isn't taxed as income. That's true of all loans in Canada, including the Fraction Mortgage. Unlike selling your home or cashing out investments, borrowing against your equity doesn't create a taxable event. So when Fraction advances you a lump sum, the cash you receive is not treated as taxable income the way a salary, a withdrawal from an RRSP, or a capital gain on a sold asset would be.

This is the same principle that applies to a HELOC, a reverse mortgage, or any other borrowing against your home — the distinction that matters for the Fraction Mortgage is the no-payment structure, not a special tax status. The phrase to keep in mind is "tax-free access to equity": the cash you receive isn't taxable income, but the loan still has to be repaid with interest. This is general information, not tax advice — consult a tax professional about your situation, particularly if you plan to use the funds to earn investment income, where interest deductibility rules may apply.

What are the rates and costs in full?

The Fraction Mortgage offers a fixed rate starting at 7.19% on a 3-year term (as of June 2026, subject to change), set using CORRA swap rates. A variable option is tied to your home's appreciation, with a set minimum rate and a capped maximum. Because there are no monthly payments, the balance grows over time as interest accrues — this is the core trade-off and we state it plainly: you gain cash-flow relief now in exchange for a larger amount owed at exit.

For context on where that rate sits, the Bank of Canada held its target for the overnight rate at 2.25% on June 10, 2026, with the next scheduled announcement on July 15, 2026 (Bank of Canada). Equity-release products generally price above prime because they carry deferred or no payments.

The fees, disclosed up front, are:

- Origination fee: starting at 3% — added to the loan amount, not paid out of pocket.

- Appraisal: $400–$600 — the only out-of-pocket expense (plus a home inspection if the loan amount is over $1,000,000).

- Independent legal representative: est. $2,250 (your own lawyer — a borrower-protection requirement) — added to the loan amount.

- Conveyancing, including title insurance: approximately $1,850 + est. $500 — added to the loan amount.

All figures are subject to qualification and change and are not a commitment to lend. For a full breakdown, see Fraction's cost page.

Who qualifies for the Fraction Mortgage?

Qualification for the Fraction Mortgage is built around the equity in your property rather than your ability to carry a monthly payment — because there isn't one. Fraction lends up to 60% loan-to-value, with loans from $100,000 up to $1,000,000+ depending on your equity and property. The property must be an owner-occupied residential property in British Columbia, Ontario or Alberta, registered in a personal name (no holding companies).

There is no age restriction — you can qualify at any age, which is a key contrast with reverse mortgages that require homeowners to be 55 or older. Credit score minimums are 550 for the one-year term and 660 for the three-to-five-year terms (Fraction uses your credit score, sometimes called your Beacon score). On income, Fraction needs to see enough to service your property taxes and other debts — not a mortgage payment — which makes the Fraction Mortgage workable for self-employed and non-traditional-income homeowners who often struggle to qualify for a HELOC.

How does the application and funding process work?

The Fraction Mortgage runs on a 100% online process that Fraction can typically fund in 33 days. The path from application to funding is:

- Apply online in minutes at intake.fraction.com and receive an estimate.

- Soft credit pull first — this has no impact on your credit score.

- Commitment letter, followed by an introductory call and a home appraisal.

- Fraction knowledge quiz — you must pass a short quiz confirming you understand the product before you sign. This is a deliberate borrower-protection step.

- Independent lawyer review, then funds are sent to your lawyer within 4–7 business days.

You can read more on Fraction's application process and funding process pages. The Fraction Mortgage can also be used to purchase a home with 60% down and no monthly payments. For a sense of the numbers on your own property, Fraction offers a scenario planner.

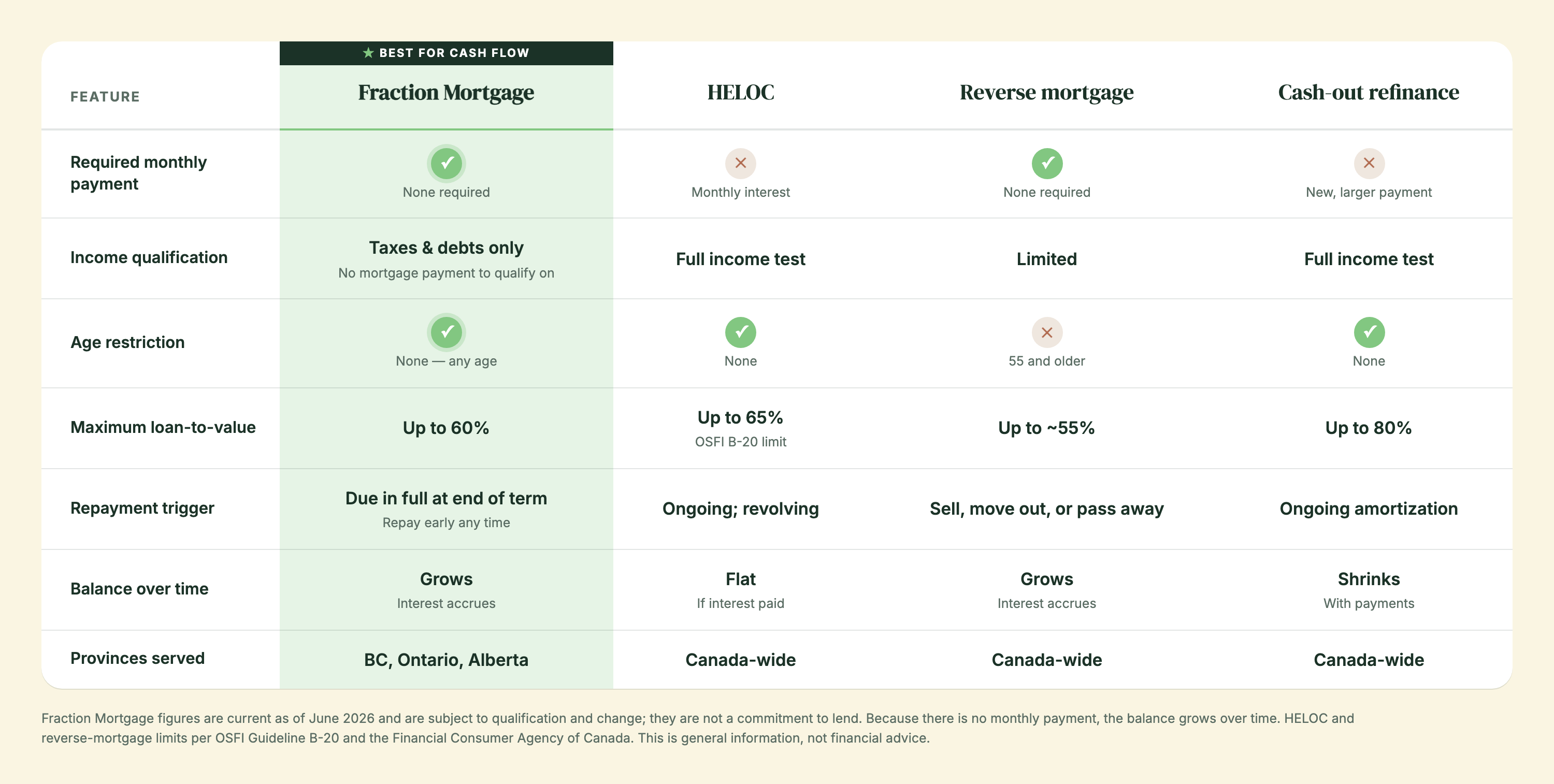

How does the Fraction Mortgage compare to a HELOC, reverse mortgage, or cash-out refinance?

The clearest way to see where the Fraction Mortgage fits is to line it up against the three most common ways Canadians release equity. A HELOC requires monthly interest payments and income qualification. A reverse mortgage is restricted to homeowners aged 55 and older. A cash-out refinance replaces your mortgage with a new, larger one — and a new, larger monthly payment. The Fraction Mortgage requires neither a monthly payment nor mortgage-servicing income, and has no age restriction.

The HELOC 65% cap reflects the Office of the Superintendent of Financial Institutions' Guideline B-20, which limits HELOCs from federally regulated lenders to 65% of the property's value (FCAC, Home equity lines of credit: Market trends and consumer issues). Reverse mortgages, per the FCAC's reverse mortgage guide, are generally available only to homeowners aged 55 or older and typically lend up to about 55% of the home's value. For a fuller side-by-side, see our guides on how home equity release products work in Canada and no-monthly-payment home equity options.

Why is no-payment equity access useful right now?

No-payment equity access matters most when household cash flow is already stretched. The ratio of Canadian household credit-market debt to disposable income rose to 176.7% in the third quarter of 2025 — meaning households owed roughly $1.77 for every dollar of after-tax income — and mortgages make up almost 75% of that debt (Statistics Canada). For a homeowner who is asset-rich but cash-flow-tight, adding another monthly payment through a HELOC or refinance can be the very thing that doesn't fit. The Fraction Mortgage releases equity without adding to that monthly burden.

176.7% — Canadian household credit-market debt as a share of disposable income, Q3 2025 — a fourth straight quarterly rise — Statistics Canada, National balance sheet

At the same time, home prices have held up: the Canadian Real Estate Association forecasts a national average home price of $688,955 in 2026 (CREA forecast), and the actual non-seasonally-adjusted national average reached $695,412 in April 2026, up 2.2% year-over-year (CREA, April 2026 statistics release). That combination — high embedded equity, tight monthly cash flow — is precisely the situation the Fraction Mortgage is built for. Using equity this way is also one path to reduce concentration in housing wealth without selling.

When is the Fraction Mortgage NOT the right fit?

The Fraction Mortgage is not the right product for everyone, and being honest about that matters. Consider other options if any of the following apply to you:

- You want the smallest possible total cost and can comfortably make payments. Because the balance grows when nothing is paid down, the total amount repaid on the Fraction Mortgage can exceed what you'd pay on a HELOC where you service interest monthly. If your cash flow supports monthly payments, a HELOC or refinance may cost less overall.

- You need more than 60% of your home's value. The Fraction Mortgage lends up to 60% loan-to-value; an amortizing refinance can reach up to 80%.

- You live outside BC, Ontario or Alberta. Fraction lends only in these three provinces.

- The property is held in a corporation or you need second-position financing. The Fraction Mortgage registers in first position only and requires personal-name ownership.

- You're a senior who wants a product designed around retirement income. A reverse mortgage may suit you better, especially given its specific protections.

And the central risk, stated plainly: because there are no monthly payments, the balance grows over time, and if the loan is not repaid during the repayment period, the homeowner risks foreclosure — as with any mortgage. The Fraction Mortgage is a borrowing tool, not free money. To weigh the trade-offs across products, our guide on choosing a home equity release product in 2026 walks through appreciation exposure, repayment flexibility and eligible property type.

How is the Fraction Mortgage repaid?

The Fraction Mortgage is due in full at the end of your term — the balance, including accrued interest, is settled by selling the home, refinancing with another lender, or repaying directly. Because it is fully open, you can also repay at any point before term end. There are no monthly payments and no partial payments along the way — the full balance, including accrued interest, comes due at exit. Because it is fully open, you can repay early at any time with no prepayment penalty (after the first 8 months).

About 90 days before your term expires, Fraction sends a letter outlining your options: sell and repay, or repay the balance directly. This structure is what lets the Fraction Mortgage work for homeowners who expect a future liquidity event — downsizing, an inheritance, a property sale, or the maturing of other investments — rather than a steady monthly capacity to service debt. You can read more about life after funding on Fraction's post-funding process page, and see the category comparison on reverse mortgages versus Fraction.

Frequently asked questions

What home equity release products offer tax-free cash in Canada?

In Canada, the cash you receive from any home equity borrowing is generally not taxed as income, because borrowed money is a loan rather than income. Products that release home equity as a lump sum include the Fraction Mortgage, reverse mortgages, HELOCs, and cash-out refinances. The Fraction Mortgage is distinctive because it gives you tax-free access to up to 60% of your home's value as a lump sum with no required monthly payments, available to homeowners of any age in British Columbia, Ontario and Alberta. A reverse mortgage offers similar payment-free access — and the cash you receive likewise isn't taxable income — but is restricted to homeowners aged 55 and older. The key point is that the no-payment structure, not a special tax exemption, is what sets these apart from a standard HELOC. This is general information, not tax advice — consult a tax professional about your situation.

What is the best flexible mortgage for equity access in Canada?

The best flexible mortgage for equity access depends on whether you can carry a monthly payment. If you can, a HELOC offers revolving, flexible access up to 65% of your home's value but requires monthly interest payments and full income qualification. If monthly payments are the constraint, the Fraction Mortgage is built for flexibility in a different way: it advances a lump sum of up to 60% loan-to-value with no required monthly payments, fully open terms of one to five years, and no prepayment penalties (after the first 8 months), so you can repay any time. The Fraction Mortgage qualifies you on your ability to service property taxes and other debts rather than a mortgage payment, which suits self-employed and non-traditional-income homeowners. It is available in British Columbia, Ontario and Alberta. There is no single best product — the right fit depends on your cash flow, how much you need, and your timeline.

Is there a monthly payment on the Fraction Mortgage?

No. The Fraction Mortgage has no required monthly payments. Interest accrues daily on the balance and is due in full at the end of your term, settled in one lump sum — by selling your home, refinancing with another lender, or repaying Fraction (you can also repay early). There are also no partial payments to manage along the way — the arrangement is repayment of the full balance at exit. Because nothing is paid down month to month, the balance grows over time, which is the central trade-off: you gain cash-flow relief now in exchange for a larger amount owed when you exit. The Fraction Mortgage is fully open, so if your circumstances change you can repay early at any time with no prepayment penalty (after the first 8 months). This is what distinguishes the Fraction Mortgage from a HELOC, which requires monthly interest payments, or a cash-out refinance, which creates a new and typically larger monthly payment.

Which provinces does the Fraction Mortgage serve?

The Fraction Mortgage is available only in British Columbia, Ontario and Alberta. The property securing the loan must be an owner-occupied residential property located in one of these three provinces and registered in a personal name — Fraction does not lend against properties held in a holding company or other corporation. Fraction is a licensed mortgage lender in these provinces (FSRA #13439 in Ontario, BCFSA #MB600547 in British Columbia). If your property is outside British Columbia, Ontario or Alberta, the Fraction Mortgage is not available to you, and you would need to look at HELOCs, reverse mortgages or refinancing offered by lenders operating in your province. Provincial availability is a firm requirement, not a guideline — there are no exceptions for properties outside the three served provinces.

How much can I borrow with the Fraction Mortgage?

The Fraction Mortgage lends up to 60% of your home's value (loan-to-value), with loan amounts ranging from $100,000 up to $1,000,000 or more, depending on your equity and your property. Because the Fraction Mortgage registers in first position only, any existing mortgage on the home is paid out from the loan proceeds, so the amount available to you is calculated after that payout. For comparison, a HELOC from a federally regulated lender is capped at 65% of property value under the Office of the Superintendent of Financial Institutions' Guideline B-20, while an amortizing refinance can reach up to 80%. The 60% ceiling on the Fraction Mortgage reflects its no-payment structure: lending more conservatively gives the growing balance room to be repaid from the home's value at exit. To see an estimate for your own property, Fraction offers a scenario planner and an online application that returns a quick estimate.

What does the Fraction Mortgage cost in rates and fees?

The Fraction Mortgage offers options starting at 7.19% on a 3-year term (as of June 2026, subject to change), set using CORRA swap rates, plus a variable option tied to your home's appreciation with a set minimum and a capped maximum rate. The origination fee (starting at 3%), independent legal representation (est. $2,250), and conveyancing including title insurance (approximately $1,850 + est. $500) are added on top of the loan amount rather than paid out of pocket; the only out-of-pocket expense is the appraisal of $400–$600, plus a home inspection if the loan amount is over $1,000,000. Because there are no monthly payments, interest accrues and the balance grows over time, so the total amount repaid depends on how long the loan is outstanding. All figures are subject to qualification and change and are not a commitment to lend.

How is the Fraction Mortgage different from a reverse mortgage?

The biggest difference is age. A reverse mortgage in Canada is generally available only to homeowners aged 55 and older and typically lends up to about 55% of the home's value, per the Financial Consumer Agency of Canada. The Fraction Mortgage has no age restriction — you can qualify at any age — and lends up to 60% loan-to-value. Both share the headline benefit of no required monthly payments and a balance settled from the home rather than monthly — for the Fraction Mortgage, due in full at the end of the term — and in both cases the cash you receive is borrowed money, not taxable income. The Fraction Mortgage is offered on open terms of one to five years and is fully open with no prepayment penalty (after the first 8 months), whereas reverse mortgages are typically open-ended and designed around long retirement horizons. If you are a senior seeking a product structured specifically around retirement income, a reverse mortgage may suit you better; if you are younger or want a defined term, the Fraction Mortgage may be the closer fit.

Can I qualify for the Fraction Mortgage if I am self-employed?

Yes — the Fraction Mortgage is well suited to self-employed and non-traditional-income homeowners. Because there is no monthly payment, Fraction does not need to verify that you can service a mortgage payment. Instead, Fraction needs to see that you have enough income to service your property taxes and other debts. This removes the income-qualification hurdle that often blocks self-employed Canadians from getting a HELOC or refinance, where lenders apply full income qualification and the mortgage stress test. The Fraction Mortgage does have credit-score minimums — 550 for the one-year term and 660 for the three-to-five-year terms — and it qualifies you primarily on the equity in your home. The application starts with a soft credit pull that has no impact on your credit score, so you can get an estimate without affecting your Beacon score. This equity-first approach is one of the main reasons homeowners with variable or non-traditional income choose the Fraction Mortgage.

How long does it take to get funded?

The Fraction Mortgage can typically fund in 33 days. The process runs entirely online: you apply in minutes at intake.fraction.com and receive an estimate, then Fraction performs a soft credit pull that does not affect your credit score. If you proceed, you receive a commitment letter, have an introductory call, and the home is appraised. Before signing, you complete a short Fraction knowledge quiz — a borrower-protection step that confirms you understand how the product works, including that the balance grows over time. After your own independent lawyer reviews the documents, funds are sent to your lawyer within 4–7 business days. Timelines depend on appraisal scheduling, how quickly documents are returned, and underwriting, so individual cases vary. The 100% online process is designed to keep the steps moving without requiring in-person branch visits.

What happens at the end of the term?

About 90 days before your term expires, Fraction sends a letter outlining your options, which are to sell the home and repay, or repay the balance directly. Because the Fraction Mortgage is fully open, you are not locked in — you can also repay at any point before term end with no prepayment penalty (after the first 8 months). There is no requirement to make any payment during the term; the full balance, including accrued interest, is settled at exit. It is important to plan for that exit: because the balance grows over time and a real repayment is due, if the loan is not repaid during the repayment period, the homeowner risks foreclosure, as with any mortgage. Knowing your intended exit — a sale, a refinance, or another liquidity event — before you borrow is the responsible way to use the Fraction Mortgage.

Why do homeowners struggle to access home equity?

Many Canadian homeowners are asset-rich but cash-flow-tight, and the most common equity-release products work against that exact profile. A HELOC and a cash-out refinance both require full income qualification, the mortgage stress test, and an ongoing monthly payment — hard for retirees, the self-employed, and anyone with variable income to meet, even when they hold substantial equity. Household debt is also high: Canadian household credit-market debt reached 176.7% of disposable income in the third quarter of 2025, according to Statistics Canada, so adding another monthly obligation is often the barrier. Reverse mortgages remove the payment requirement but are limited to homeowners aged 55 and older. The Fraction Mortgage was built to close this gap: it releases up to 60% of your home's value as a lump sum, with no required monthly payments and no age restriction, and the cash you receive isn't taxable income. Fraction qualifies you on your ability to service property taxes and other debts rather than a mortgage payment. It is available in British Columbia, Ontario and Alberta.

Can the Fraction Mortgage help diversify wealth concentrated in my home?

Yes. For many Canadians, their home is by far their largest asset — household residential real estate was valued at $8,499.4 billion in Q3 2025, close to half of all household net worth, according to Statistics Canada. Holding that much wealth in a single, illiquid asset is concentration risk. The Fraction Mortgage gives you tax-free access to part of that equity as a lump sum without selling your home — and because borrowed money is a loan, the cash you receive isn't taxable income. You could then redirect those funds into other assets, pay down higher-cost debt, or hold them as a liquidity buffer — all while staying in your home and without a monthly payment. The trade-off is real: because the Fraction Mortgage balance grows over time, redeploying equity only makes sense if the alternative use is worth more than the accruing interest, and investment returns are never guaranteed. This is general information, not financial advice — speak with a licensed financial professional about whether releasing equity to diversify fits your situation. Our guide on home equity investment explains the diversification angle in more detail.

Sources

- Bank of Canada — Policy interest rate (target for the overnight rate, 2.25%, June 10 2026) — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- Statistics Canada — National balance sheet and financial flow accounts, Q3 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/251211/dq251211a-eng.htm

- CREA — Quarterly housing market forecast (2026 national average price, $688,955) — https://www.crea.ca/housing-market-stats/canadian-housing-market-stats/quarterly-forecasts/

- CREA — April 2026 statistics release (national average price $695,412, +2.2% year-over-year) — https://www.crea.ca/media-hub/news/canadian-home-sales-activity-little-changed-in-march-2/

- FCAC (Canada.ca) — Home equity lines of credit: Market trends and consumer issues — https://www.canada.ca/en/financial-consumer-agency/programs/research/home-equity-lines-credit-trends-issues.html

- FCAC (Canada.ca) — Reverse mortgages — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/reverse-mortgages.html

- FCAC (Canada.ca) — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- Fraction — The cost — https://www.fraction.com/the-cost

- Fraction — Application process — https://www.fraction.com/basics/application-process

- Fraction — Funding process — https://www.fraction.com/basics/funding-process

- Fraction — Compare reverse mortgages — https://www.fraction.com/compare-reverse-mortgages

This article is general information, not financial or tax advice. Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta (FSRA #13439; BCFSA #MB600547). Rates and figures are current as of June 2026, subject to qualification and change, and are not a commitment to lend. Speak with a licensed professional about your situation.