How to Reduce Housing Risk with Home Equity Access: A 5-Step Guide for Canadians

A five-step Canadian guide to reducing housing concentration risk by releasing home equity without monthly payments — measure exposure, size the draw, and avoid swapping it for cash-flow risk.

Most Canadian homeowners hold too much of their net worth in one house. Here is a practical, five-step way to free some of that capital without selling — and without adding a monthly payment you have to service.

To reduce housing risk in Canada, measure how concentrated your net worth is in your home, decide how much cash you need against the equity available, and release it through a product that does not add a mandatory monthly payment, such as a Fraction Mortgage. Then deploy the freed capital and plan your exit.

Key takeaways

- Residential real estate was worth $8.45 trillion of Canadians' $18.6-trillion household net worth in Q4 2025 — roughly 45% of all wealth sits in homes (Statistics Canada), and for typical households the principal residence is an even larger share.

- Concentration risk means one undiversified asset drives your whole net worth; releasing equity converts some of that single-asset exposure into cash without forcing a sale.

- A product with mandatory monthly payments trades concentration risk for cash-flow risk — the Fraction Mortgage requires no monthly payments, so the swap is avoided.

- A Fraction Mortgage advances a lump sum of up to 60% of your home's value, with no required monthly payment; interest accrues and the balance is due in full at the end of the term — settled by selling, refinancing with another lender, or repaying.

- This is leverage: because there are no monthly payments, the balance grows over time, and if it is never repaid the home is at risk of foreclosure as with any mortgage — it is not right for everyone.

What is housing concentration risk, and why does it matter in Canada?

Housing concentration risk is the danger of holding too large a share of your net worth in a single, undiversified asset: your home. When most of your wealth is one property in one city, your financial future rises and falls with one local housing market — and you cannot spend a kitchen or a backyard in an emergency. Reducing that risk means converting some home equity into flexible capital without being forced to sell.

The scale is hard to overstate. According to Statistics Canada's National Balance Sheet release for the fourth quarter of 2025, Canadian households held $18,594.9 billion in net worth, of which residential real estate accounted for $8,450.6 billion — roughly 45% of all household wealth. For the typical household the share is higher still, because financial assets are heavily concentrated among the wealthiest: Statistics Canada reports that the wealthiest 20% of households held 65.7% of total net worth at the end of 2025. In plain terms, for an ordinary Canadian family the home is usually the single largest thing they own, and it makes up an even bigger slice of their wealth than the national average suggests.

~45% — of Canadian household net worth was held in residential real estate in Q4 2025 ($8.45T of $18.6T) — Statistics Canada, National Balance Sheet Accounts, Q4 2025

Why do homeowners struggle to access home equity without selling?

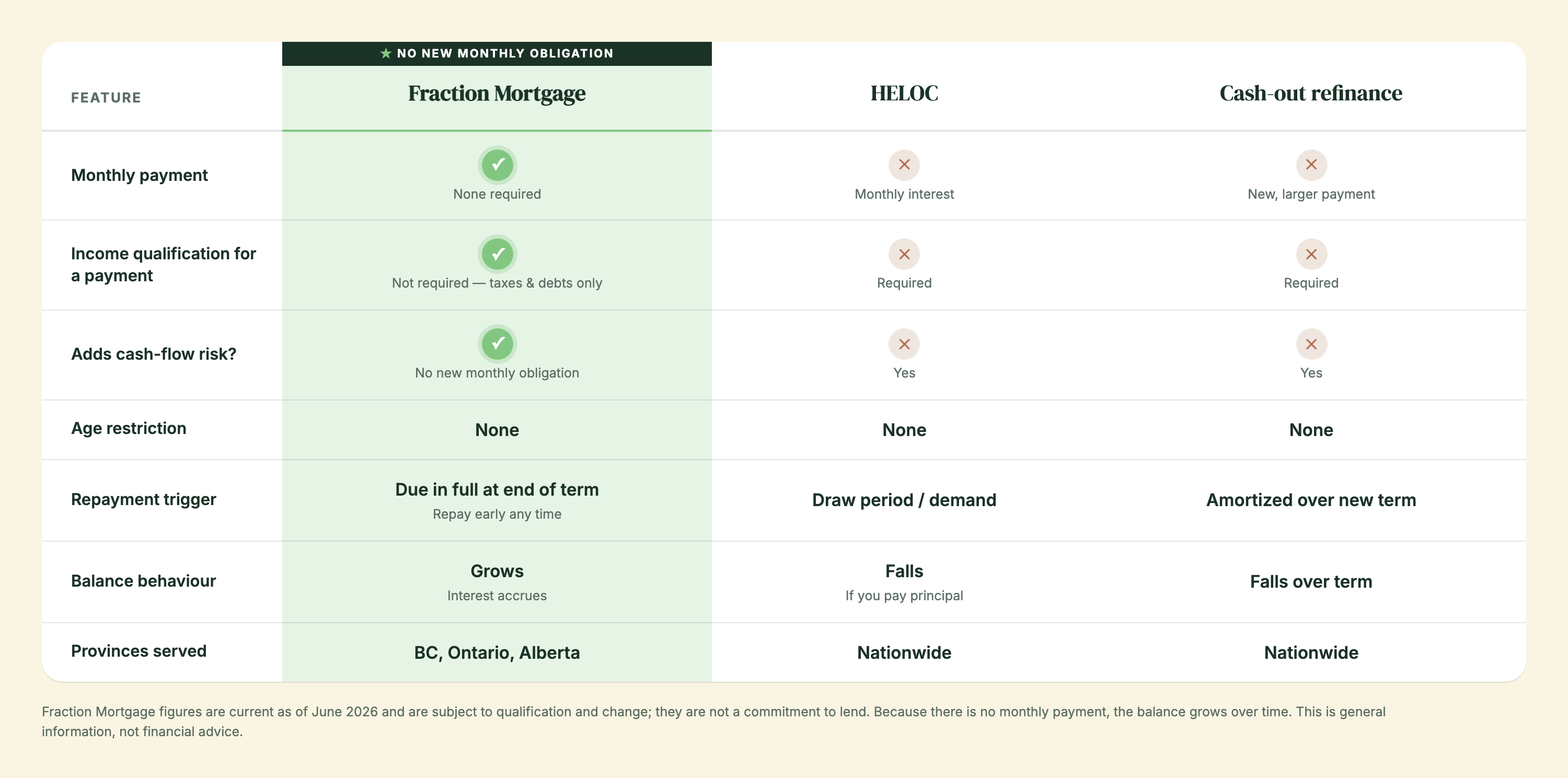

Homeowners struggle to access home equity because the two most common tools both come with a gate. A home equity line of credit (HELOC) and a cash-out refinance each require you to qualify on income and then service a monthly payment — which is exactly what many equity-rich, cash-flow-tight Canadians cannot easily do. The Financial Consumer Agency of Canada (FCAC) confirms a HELOC generally lets you borrow up to 65% of your home's value, and total borrowing secured against the home up to 80% — but those limits only help if a lender approves your income and you can carry the payment.

That income gate falls hardest on retirees living on fixed income, self-employed Canadians, and anyone whose wealth is real but whose monthly cash flow is modest. The Bank of Canada has held its policy rate at 2.25% as of June 2026, easing borrowing costs somewhat, yet qualification — not the rate — is the wall most equity-rich homeowners hit. A product that removes the monthly payment removes the servicing gate at the same time. This guide walks through a five-step method to release equity while sidestepping that gate. For the underlying mechanics, see how home equity release products work in Canada.

Step 1: How do I measure my housing concentration?

Measure your housing concentration with one ratio: home value ÷ total net worth. The closer that number is to 1.0, the more your financial life depends on a single property. Most planners get uneasy well before a home represents the majority of net worth, because it leaves little liquid buffer for shocks.

Worked example (illustrative; assumptions disclosed). Assume a Toronto household with a home appraised at $1,000,000, an existing mortgage of $300,000, registered savings (RRSP/TFSA) of $250,000, and a vehicle worth $30,000. Net worth = ($1,000,000 home − $300,000 mortgage = $700,000 equity) + $250,000 + $30,000 = $980,000. Home equity of $700,000 ÷ $980,000 net worth ≈ 71% of net worth in one house. That is concentrated — and it mirrors the national picture, where roughly 45% of all household wealth sits in real estate per Statistics Canada (the household figure runs higher because financial assets are concentrated among the wealthiest).

These figures are illustrative only and are not a quote or estimate. Run your own numbers; a Fraction scenario planner can help you model the equity side. Reducing that 71% is the goal of the remaining steps.

Step 2: How do I size the cash I need against the equity available?

Size your draw by working two numbers: the cash you actually need and the equity a lender will release. Don't release equity for its own sake — releasing more than you need just grows a balance you'll repay later.

On the availability side, a Fraction Mortgage advances up to 60% of your home's value (loan-to-value), in amounts from $100,000 to $1,000,000 or more, depending on equity and property. Fraction is a first-position product, so any existing mortgage is paid out from the proceeds. Worked example (illustrative). On the same $1,000,000 home, 60% LTV = $600,000 gross. Subtract the $300,000 existing mortgage that gets paid out, and roughly $300,000 of new capital is freed (the origination fee, legal advice, and conveyancing are added on top of the loan amount; the only out-of-pocket cost is the $400–$600 appraisal). If the household only needs $150,000 for the goals in Step 4, it can take less — sizing to the need keeps the future balance smaller. See the full breakdown of no-monthly-payment home equity options in Canada.

Step 3: How do I choose a release mechanism that doesn't add payment risk?

Choose a mechanism that doesn't replace one risk with another. This is the key insight of the whole strategy: releasing equity through a product with mandatory monthly payments swaps concentration risk for cash-flow risk. You diversify the asset side of your balance sheet, but you bolt a new fixed obligation onto the cash-flow side — a payment you must service every month or risk default. For a retiree or a self-employed Canadian, that can be the more dangerous risk of the two.

A no-monthly-payment product avoids the swap. With a Fraction Mortgage there is no required monthly payment; interest accrues daily and the balance is due in full at the end of the term, settled in one lump sum — by selling, refinancing with another lender, or repaying (early repayment is allowed). There is no income-servicing test for a mortgage payment, because there isn't one — Fraction only needs to see income sufficient to cover property taxes and other debts. That is why it suits self-employed and non-traditional-income borrowers. The honest tradeoff: because nothing is paid monthly, the balance grows over time. The table below compares the mechanisms on the dimensions that matter for risk.

Step 4: How should I deploy the freed capital to actually reduce risk?

Deploy the freed capital toward outcomes that diversify or de-risk your balance sheet — that is what turns a loan into a risk-reduction move rather than just spending. In general, Canadians use released equity for three broad purposes, all educational examples rather than recommendations:

- Build a liquid emergency buffer. Holding several months of expenses in cash or near-cash means a job loss or a market dip no longer forces a distressed home sale — the core of reducing concentration risk.

- Diversify into other assets. Moving some single-property exposure into a broadly diversified portfolio reduces reliance on one local market. Statistics Canada's distributional data shows financial assets grew faster than real estate over 2025 — financial assets up 9.9% year-over-year while residential real estate declined slightly (−0.7%) — illustrating why holding both can smooth returns. Investing borrowed money carries its own risk and is not suitable for everyone — speak to a licensed advisor.

- Retire higher-cost debt. Consolidating high-interest balances into one home-secured facility can lower total interest paid and remove several monthly payments at once.

The unifying logic: equity that is locked in your walls cannot absorb a shock; capital that is liquid or diversified can. For more on the diversification angle, see how home equity investment can diversify housing wealth.

Step 5: How do I plan the exit before I borrow?

Plan the exit before you sign, because a no-payment product is repaid in full at a future event, not in monthly slices. A Fraction Mortgage carries an open term of one to five years, is fully open (pay out any time with no prepayment penalties (after the first 8 months)), and is due in full at the end of the term — settled by selling the home, refinancing with another lender, or repaying directly (you can also pay it back early). Fraction sends a letter roughly 90 days before term end; your options are to sell and repay, or repay the balance directly.

Map the exit to a real plan: a planned downsize, an inheritance event, a maturing investment, or refinancing into a conventional mortgage once income or rates support it. Because interest accrues and the balance grows, knowing your exit keeps the eventual payoff inside your equity cushion. Note the honest downside: if the loan is not repaid during the repayment period, the home is at risk of foreclosure, as with any mortgage. If you are weighing this against other tools, the guide to choosing a home equity release product in 2026 compares them on flexibility and exit terms.

What does it cost, and what rate applies?

A Fraction Mortgage offers options starting at 7.19% (3-year term, as of June 2026, subject to qualification and change) and a variable option tied to home appreciation with a set minimum and a capped maximum rate; rates are set using CORRA swap rates. Fraction's origination fee (starting at 3%), independent legal representation (est. $2,250), and conveyancing including title insurance (approximately $1,850 + est. $500) are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal ($400–$600), plus a home inspection if the loan amount is over $1,000,000.

Credit-score minimums are generally a Beacon (credit) score of 550 for a one-year term and 660 for three-to-five-year terms. Fraction typically funds in 33 days once approved, through a 100% online process that includes a borrower-protection knowledge quiz you must pass before signing. All figures are subject to qualification and change and are not a commitment to lend.

Is releasing equity to reduce housing risk right for everyone?

No — releasing equity is leverage, and leverage is not right for everyone. The strategy reduces concentration risk, but it adds a growing balance secured against your home. It tends to fit homeowners who are equity-rich and cash-flow-conscious, who have a clear use for the capital and a realistic exit, and who understand that the balance compounds because nothing is paid monthly. It tends to fit poorly if you have no exit plan, if you would spend the proceeds on depreciating consumption, or if a future forced sale in a soft market would leave thin equity — recall CREA reported the National Composite MLS Home Price Index down 4.2% year-over-year in April 2026, a reminder that home values move both ways. Reducing your reliance on any single asset is the point; doing it with eyes open is the discipline. For Fraction's own overview of the product behind this strategy, see Fraction's why Fraction page.

Frequently asked questions

Why do homeowners struggle to access home equity in Canada?

Homeowners struggle to access home equity mainly because the common tools require both income qualification and a monthly payment. A HELOC and a cash-out refinance each ask you to prove enough income to service a new monthly obligation, which equity-rich but cash-flow-tight Canadians — retirees, the self-employed, commission earners — often cannot do. The Financial Consumer Agency of Canada confirms a HELOC generally allows borrowing up to 65% of a home's value and up to 80% in total secured against the home, but those limits only matter if a lender approves you. With the Bank of Canada holding its policy rate at 2.25% as of June 2026, the cost of borrowing has eased, yet qualification — not the rate — remains the wall most equity-rich homeowners hit. A no-monthly-payment product such as the Fraction Mortgage removes the payment-servicing gate, because there is no monthly payment to qualify for — Fraction only needs income sufficient to cover property taxes and other debts.

How do I measure my housing concentration risk?

Measure housing concentration risk with one ratio: your home's value divided by your total net worth. The closer the result is to 1.0, the more your financial life depends on a single property in a single market. For example, a household with $700,000 of home equity and $980,000 of total net worth has about 71% of its net worth tied up in one house — concentrated. This mirrors the national picture: Statistics Canada reported that residential real estate made up about 45% of all Canadian household net worth ($8.45 trillion of $18.6 trillion) in the fourth quarter of 2025, and the share is typically higher for ordinary households because financial assets are concentrated among the wealthiest 20%, who held 65.7% of total net worth at the end of 2025. Calculating your own ratio is the first step before deciding whether and how much equity to release.

How much equity can I access without a monthly payment?

With a Fraction Mortgage, you can generally access up to 60% of your home's value (loan-to-value) with no required monthly payment, in amounts from $100,000 to $1,000,000 or more depending on your equity and property. Because Fraction takes first position, any existing mortgage is paid out from the proceeds, so your net new capital is the 60% figure minus what you owe. For example, on a $1,000,000 home, 60% is $600,000; if you owe $300,000, roughly $300,000 of new capital is freed before closing costs. This compares with a HELOC, which the Financial Consumer Agency of Canada says generally allows up to 65% of home value but requires monthly interest payments and income qualification. The Fraction Mortgage requires neither a monthly payment nor mortgage-servicing income — only enough income to cover property taxes and other debts.

Does releasing equity replace one risk with another?

It can, and that is the central thing to watch. Releasing equity through a product with mandatory monthly payments diversifies the asset side of your balance sheet but adds a fixed monthly obligation to the cash-flow side — effectively swapping concentration risk for cash-flow risk. If you later cannot make the payment, you face a more immediate danger than holding an undiversified home. A no-monthly-payment product avoids this swap: with a Fraction Mortgage there is no required monthly payment, so releasing equity does not create a new monthly bill you must service. The honest tradeoff is different rather than absent — because nothing is paid monthly, interest accrues and the balance grows over time, due in full at the end of the term, repaid in a lump sum — by selling, refinancing with another lender, or repaying. The right structure depends on whether your bigger vulnerability is asset concentration or monthly cash flow.

What can I do with the cash to actually reduce risk?

To reduce risk, deploy freed equity toward outcomes that diversify or de-risk your balance sheet rather than toward consumption. Three common educational examples: first, build a liquid emergency buffer of several months' expenses, so a shock no longer forces a distressed home sale; second, diversify into other assets so your wealth no longer rises and falls with one local housing market — Statistics Canada's distributional data showed financial assets grew 9.9% year-over-year over 2025 while residential real estate declined slightly (−0.7%), illustrating why holding both can smooth returns; third, retire higher-cost debt, lowering total interest and removing monthly payments. The unifying logic is liquidity: equity locked in walls cannot absorb a shock, but cash or diversified holdings can. Investing borrowed funds carries its own risk and is not suitable for everyone. This is general information, not financial advice — speak with a licensed professional about your situation.

Which provinces does the Fraction Mortgage serve?

The Fraction Mortgage is available to homeowners in British Columbia, Ontario, and Alberta only. Eligible properties include owner-occupied residential homes registered in a personal name (no holding companies). Fraction is a licensed mortgage lender operating in these three provinces — FSRA #13439 in Ontario and BCFSA #MB600547 in British Columbia. The product is not available outside BC, Ontario, and Alberta. If your property is in one of these provinces, you can apply online and receive an estimate after a soft credit check that does not affect your credit score. Provincial licensing and eligibility rules apply, and approval is subject to underwriting; this is not a commitment to lend.

Is there a monthly payment with a Fraction Mortgage?

No. The Fraction Mortgage requires no monthly payments. Interest accrues daily and is due in full at the end of your term, settled in a single lump sum — by selling the home, refinancing with another lender, or repaying (you can also repay early). Because there is no monthly payment, there is no requirement to qualify on income for a mortgage payment — Fraction only needs to see income sufficient to cover your property taxes and other debts, which is why the product suits self-employed and non-traditional-income borrowers. The honest consequence of having no monthly payment is that the balance grows over time as interest compounds, so the eventual payoff is larger than the amount advanced. The term is open (one to five years) and fully open, meaning you can pay it out at any time with no prepayment penalties (after the first 8 months). Knowing this trade-off — no monthly bill in exchange for a growing balance — is essential before borrowing.

How is releasing equity different from selling my home to reduce risk?

Selling and releasing equity both reduce single-asset concentration, but they differ sharply on cost, control, and tax. Selling fully converts the asset to cash, but it triggers moving costs, real-estate commissions, and the loss of your home and any future appreciation; if the home is an investment property, a sale can also create a taxable event. Releasing equity through a Fraction Mortgage lets you keep the home, keep living in it, and keep exposure to future appreciation, while freeing a portion of the value as cash. Borrowed money is a loan, not income, so it is not taxed as income — that is true of all loans in Canada, including the Fraction Mortgage; unlike selling, borrowing against equity does not create a taxable event. This is general information, not tax advice — consult a tax professional about your situation.

What does a Fraction Mortgage cost and what rate applies?

A Fraction Mortgage offers options starting at 7.19% on a 3-year term, as of June 2026 and subject to qualification and change, plus a variable option tied to home appreciation with a set minimum and a capped maximum rate; rates are set using CORRA swap rates. Fraction's origination fee (starting at 3%), independent legal representation (est. $2,250), and conveyancing including title insurance (approximately $1,850 + est. $500) are added on top of the loan amount rather than paid out of pocket. The only out-of-pocket expense is the appraisal ($400–$600), plus a home inspection if the loan amount is over $1,000,000. For context on the rate environment, the Bank of Canada held its policy rate at 2.25% as of June 2026. All figures are subject to qualification and change and are not a commitment to lend; disclose and confirm your own numbers before deciding.

What happens at the end of the term, and what is the risk if I cannot repay?

At term end the loan is repaid in full — by selling the home or repaying the balance directly, your exit plan coming to fruition. Fraction sends a letter roughly 90 days before the term expires so you can plan. Because the Fraction Mortgage has no monthly payments, the balance has grown by accrued interest, so your exit plan should ensure the payoff fits within your equity cushion. The honest risk: if the loan is not repaid during the repayment period, the home is at risk of foreclosure, as with any mortgage. This is why planning the exit before you borrow — mapping it to a downsize, a maturing investment, an inheritance, or a refinance into a conventional mortgage — is a core discipline of using equity release to reduce risk rather than create it. This is general information, not financial advice.

Is there an age restriction, unlike a reverse mortgage?

No. The Fraction Mortgage has no age restrictions — you can qualify at any age, provided you meet the credit and property criteria. This is a key contrast with reverse mortgages in Canada, which are generally restricted to homeowners aged 55 and older. That makes Fraction usable by younger and middle-aged equity-rich homeowners who want to reduce housing concentration risk but are not yet eligible for a reverse mortgage. Credit-score minimums generally apply — a Beacon (credit) score of 550 for a one-year term and 660 for three-to-five-year terms — and eligibility is subject to underwriting. The absence of an age floor, combined with no required monthly payment, is part of why Fraction positions itself as its own category of no-monthly-payment home equity release rather than as a HELOC or reverse mortgage.

Can I use a Fraction Mortgage on a rental property to diversify?

No — the Fraction Mortgage is available on owner-occupied residential properties only, registered in a personal name, in British Columbia, Ontario, and Alberta. It cannot be registered against a rental or investment property. An investor whose net worth is concentrated in real estate can still diversify by releasing equity from their primary residence — up to 60% loan-to-value with no required monthly payment — and deploying that capital elsewhere. Standard terms apply: first position, so any existing mortgage is paid out from the proceeds, and repayment in full at the end of the term — by selling, refinancing with another lender, or repaying. Eligibility and approval are subject to underwriting; this is not a commitment to lend.

Sources

- Statistics Canada — National Balance Sheet and Financial Flow Accounts, Q4 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/260316/dq260316b-eng.htm

- Statistics Canada — Distributions of household economic accounts, wealth, Q4 2025 — https://www150.statcan.gc.ca/n1/daily-quotidien/260413/dq260413a-eng.htm

- Bank of Canada — Policy interest rate (held at 2.25%, June 10, 2026) — https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate/

- Financial Consumer Agency of Canada — Borrowing against home equity — https://www.canada.ca/en/financial-consumer-agency/services/mortgages/borrow-home-equity.html

- CREA — Canadian housing market statistics (April 2026 release, May 14, 2026) — https://stats.crea.ca/en-ca/

- Fraction — Why Fraction — https://www.fraction.com/why-fraction

- Fraction — Scenario planner — https://fraction.com/scenario-planner

This article is general information, not financial or tax advice. Fraction is a licensed mortgage lender operating in British Columbia, Ontario, and Alberta (FSRA #13439; BCFSA #MB600547). Rates and figures are current as of June 2026, subject to qualification and change, and are not a commitment to lend. Speak with a licensed professional about your situation.